Now all AAA Australian members can use their 16 digit membership number to secure a 5% discount. Along with using your PayPal account you can save 7% on your next car rental excess insurance policy with Tripcover and Allianz Global Assistance

Category Archives: Thrifty

Do your research to avoid car rental shocks

Rental cars are costly. If the upfront hire fees aren’t enough, there are lots of other charges that can double the cost. That can be anything from increased insurance costs to reduce excesses, to hiring a child seat.

If you know how the system works, however, it’s possible to minimise costs.

If you’re booking a hire car, the first thing to do is to use comparison engines that list more than one rental car company……more>

Company Policy Now Available

Now your company can cover ALL the eligible aged drivers employed in your company.

Yes, that’s right, why pay the car rental company’s expensive corporate excess insurance rate when you can use Tripcover’s much cheaper car rental excess insurance.

Simply have the car rental agreement in your company’s name and away you go.

Reduce your corporate rate with the car rental company and save. Just let them know that

you do not need their CDW or Collision Damage Waiver to cover your company’s excess

anymore and each time you take a rental out get one of our policies for the employee.

Clarifying Your Car Rental Insurance Choices

When renting a car in Australia or New Zealand, it is very important to have quality car rental excess insurance coverage for the vehicle. You have several options available, and by comparing and contrasting the different types of insurance, you can have a better idea of what you might need.

Credit Card

Many times, the credit cards you already have in your wallet will actually have collision coverage included on them. If you choose the right credit card to pay for the rental, you could actually receive coverage with zero deductible, or at least a very low deductible. This is quite different from the high cost of insurance through the car rental companies. The right card has the potential to provide coverage for the costs for which you might be liable, such as damage to the car, or even a theft but a lot of times does not cover the general exclusions such as windscreen, tyres, single vehicle accidents or undercarriage damage.

Another issue is that some that use this method of coverage for their rental vehicles have is that it can be a hassle to deal with the credit card companies. Still, given the amount that you could possibly save in the event of an accident, it does make sense at least to consider utilizing credit card coverage for the rental.

Make sure that your credit card company offers this type of coverage, as some do and some do not. Look through the policies regarding the coverage it offers, and make sure it is applicable in Australia or New Zealand – or any country you might be visiting for that matter.

Standard Travel Insurance

In some cases, you may also have collision coverage available through your travel company. If you buy a travel insurance policy for your vacation through many companies in Australia and New Zealand, you will have the option of adding on insurance for your car rentals. However, it is important to make sure that the travel insurance policy that you are considering using actually cover all the normal exclusions that the car rental companies exclude, such as windscreens and single vehicle accidents.

Dedicated Car Rental Excess Insurance

Of course, there’s always the option of buying your car rental excess cover (usually called CDW or Collision Damage Waiver) from the car rental company. This is something they will actually encourage you to do. It’s a simple solution since you can do it right at the counter. However, that does not necessarily mean it is the best solution. The cost of the insurance through the company is expensive, and could be close to the cost of the rental itself, which could double your overall expenditure. When you buy insurance through the rental company, you should not think that it will automatically cover the entire cost of damage or theft. Look at what your excess or deductible will be. It can be in the thousands in many cases. Car rental companies will sometimes offer an additional form of coverage that will drop the deductible to zero. Of course, this adds to the cost of your rental substantially.

Dedicated car rental excess cover is also offered now by such companies as Tripcover and this can be less than half the cost of the car rental companies’ rates.

However there is also the hassle of making a claim with their insurance provider Allianz Global Assistance in the event of an accident.

Take the time to research all of your options for your car rental insurance, and then choose the one that makes the best financial sense for you.

Resources:

https://www.ricksteves.com/travel-tips/transportation/car-rental-cdw

http://www.tripadvisor.com.au/ShowTopic-g255103-i531-k5982489-Car_rental_excess_reduction_Tripcover-Perth_Greater_Perth_Western_Australia.html

ANZ Car Rental Cover – leaves you exposed to excess risk

Reply

Many people use their credit cards to cover their rental car excess. Renters assume that they are fully covered, but are they really?

Let’s have a closer look at ANZ’s actual car rental cover policy, which a Tripcover customer brought to our attention, asking if they should still take out a Tripcover policy or use the ANZ rental car coverage.

What’s covered and what not by ANZ credit cards?

Here’s the thing, most of the large car rental companies, such as Thrifty, have what they describe as a “standard excess”. This excess covers basic damage to the car if it involved in a multi car accident or is stolen, for example. Though there are a number of items not included in the standard excess, and that’s the loophole in credit card travel insurance.

Hence it becomes a problem for anyone who is relying on their ANZ credit card insurance (or other credit cards aswell) because items such as windscreens, tyre damage, undercarriage damage are not considered to actually be part of the excess.

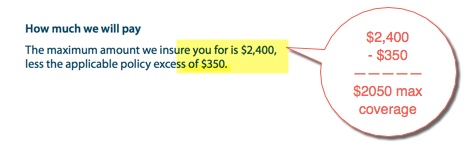

On top of that, most rental firms in Australia have an excess amount between $3500 and $4000. The ANZ car rental cover falls short by nearly $2000.

ANZ only covers $2050 excess.

The above screen grab from the ANZ Car Rental Cover terms and conditions, shows the maximum excess insured is just $2400, minus the applicable policy excess, leaves the rental customer will only $2050 maximum coverage. So if the rental car excess is $4000, then there is a gap of $1950 to pay. Ouch!

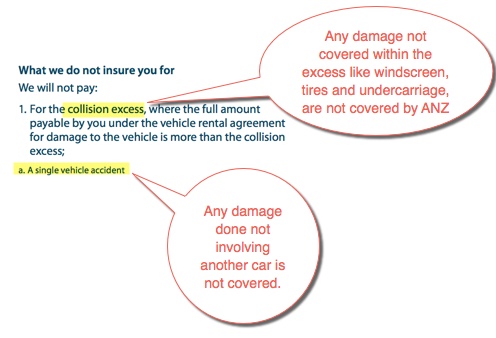

Single Vehicle Accidents are not covered by ANZ

In the above screen grab from ANZ’s terms and conditions, you will notice two things. Firstly that the coverage only includes items covered under the collision excess, and as mentioned earlier there are multiple items that rental companies do not include in their excess, but still charge you for, like windscreen and tyre damage etc.

Secondly you’ll notice that Single Vehicle accidents aren’t covered by the ANZ policy, which effectively means, if you damage the car in a car park against a static item or you hit a kangaroo on the open road, you wont be covered because there is only one vehicle involved in the accident, namely you!

As we previously wrote in our blog post about the pros and cons of car rental insurance via credit cards, there are benefits to using credit cards, especially if you choose the right credit card to pay for the rental, you could actually receive coverage with zero deductible. That being said, its worth looking into the detail, as we have done here with ANZ, to really understand what level of coverage you do have, as opposed to assuming you’re covered, and then being surprised when there is a sizable gap in the coverage.

Seinfeld gets a Rental Car

For everyone that has rented a car in the past or are going to rent a car in the future you might like this little skit from Seinfeld: